Loss of Earnings is one of the most significant components of a personal injury damages claim under the Road Accident Fund (RAF) regime. Attorneys understand the litigation pathway, and medical experts understand the clinical impact. But turning the underlying facts into a defensible financial model—one capable of withstanding scrutiny in mediation or at trial—falls squarely within the actuary’s domain. Quantifying future loss of earnings requires a precise, structured, and evidence-driven approach, with each assumption grounded in both economic reality and expert opinion.

Understanding What Loss of Earnings Measures

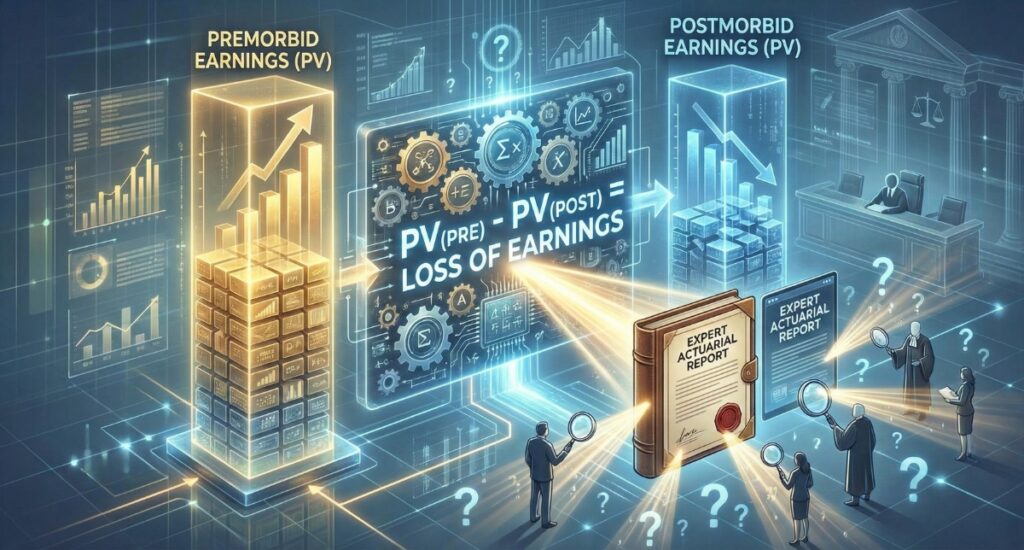

At its core, Loss of Earnings represents the difference between what a claimant would have earned had the accident not occurred and what they can realistically expect to earn after the accident. Actuaries compare two detailed monetary projections—the premorbid scenario and the postmorbid scenario—and discount the future cashflows to present value. The final result reflects the claimant’s true long-term financial loss.

Building the Premorbid Earnings Model

The first step is to establish the claimant’s premorbid earning potential. This involves examining their employment history, past payslips, tax returns, employment contracts, and any available records that help determine a realistic pre-accident income level. From there, the actuary considers how the claimant’s career would likely have progressed. That includes assumptions about promotion timing, earning potential within their industry, historical income progression patterns, and the broader economic environment in which they would have been working.

Premorbid modelling also accounts for likely retirement ages, which typically fall around 65 for males and between 60 and 65 for females, unless the evidence convincingly suggests otherwise. For individuals who were unemployed, informally employed, or still in school, the actuary constructs a hypothetical but reasonable career path based on market norms, education levels, and occupation-specific earnings benchmarks.

Establishing the Postmorbid Scenario

Once the premorbid model is established, the actuary turns to the claimant’s post-accident earning ability. This analysis depends heavily on input from medical and vocational experts such as orthopaedic surgeons, occupational therapists, industrial psychologists, and neuropsychologists. Their reports help determine the claimant’s functional limitations, employability, productivity, and potential career trajectory after the accident.

The postmorbid model may show reduced productivity, limited access to certain occupations, slower or restricted career progression, or in severe cases, total unemployability. In some matters, the claimant’s projected retirement age must be adjusted downward due to injury-related constraints or increased vulnerability in the labour market. The actuary integrates all these findings to produce a realistic financial representation of the claimant’s post-accident earning potential.

Applying Growth Rates Responsibly

A critical step in both models is applying the correct income growth rates. Earnings seldom remain static; they change due to inflation, real economic growth, and career progression. Actuaries therefore distinguish between nominal growth (which includes inflation) and real growth (which represents increases above inflation). Properly applying these growth rates is essential because even small variations can materially affect the final damages figure. A mis-stated growth assumption can lead to underestimation or overestimation of the claimant’s true future loss.

“Medical evidence tells the story of the injury. A quality actuarial report secures the story of the future.”

Discounting Future Earnings to Present Value

Future earnings cannot be compared meaningfully without discounting them to present value. The discount rate reflects inflation expectations, interest rate forecasts, and long-term economic stability. Because damages are paid today for income that would have accrued in the future, discounting ensures compensation is fair and economically neutral. A change of even one percent in the discount rate can shift the final award significantly, which is why precise and defensible assumptions are essential.

The Role of Contingencies

Contingencies are the final adjustment in the LOE calculation and represent real-world uncertainties that affect earning potential. Premorbid contingencies account for the risks the claimant would have faced without the accident, including illness, voluntary career changes, unemployment cycles, and general economic fluctuations. Postmorbid contingencies are typically higher because the injured claimant faces increased uncertainty, reduced resilience in the labour market, and greater vulnerability to job loss or stagnation.

Courts commonly apply premorbid contingencies in the range of five to fifteen percent and postmorbid contingencies between fifteen and thirty-five percent, depending on the facts. However, every case is unique, and the actuary must tailor these adjustments to the specific circumstances and the supporting evidence.

Combining the Models into a Final Calculation

With all assumptions, projections, and adjustments in place, the actuary completes the calculations by comparing the present value of premorbid earnings against the present value of postmorbid earnings. The difference between these two figures represents the claimant’s Loss of Earnings. This result is summarised in a formal expert actuarial report, which must be sufficiently transparent, defensible, and aligned with the evidence so it can withstand scrutiny from opposing actuaries, legal teams, mediators, and the court.

Why Attorneys Benefit from High-Quality Actuarial Input

In RAF matters, the numbers often drive the negotiations and trial outcomes. A strong actuarial report provides clarity, reduces uncertainty, strengthens settlement positions, and anticipates challenges that may arise during joint minutes or cross-examination. Conversely, incomplete or poorly reasoned actuarial work can weaken a case, lead to undervalued settlements, or collapse under judicial scrutiny.

Attorneys who provide complete and organised instructions—such as employment records, medical and vocational reports, and academic documents—equip the actuary to produce a more accurate and defensible report. High-quality input produces high-quality modelling, which in turn supports better litigation outcomes.

Final Thoughts

Quantifying Loss of Earnings in RAF claims requires more than inserting numbers into a formula. It is a disciplined, evidence-based modelling process that blends economic principles, vocational evidence, long-term forecasting, legal considerations, and actuarial judgment. Attorneys who understand this process are better positioned to interpret expert reports, identify weaknesses in opposing calculations, and negotiate from a position of strength. In a system where financial compensation shapes a claimant’s future stability, precision is not optional—it is essential.